When you sign a contract-whether it’s buying software, hiring a contractor, or merging two companies-you’re not just agreeing on price or delivery dates. You’re also deciding who pays if something goes wrong. That’s where liability and indemnification come in. These aren’t just legal buzzwords. They’re the backbone of how businesses protect themselves when things don’t go as planned.

What Indemnification Actually Means

Indemnification is a simple idea with complex consequences: one party agrees to pay for the other party’s losses. If your supplier’s faulty code causes a data breach, and your customers sue you, an indemnification clause says the supplier must cover your legal bills, settlements, and even the cost of notifying affected users. It’s not about blame-it’s about who’s on the hook financially.

This isn’t optional in most business deals. According to legal analysts, indemnification clauses appear in nearly all commercial agreements. They’re not just standard-they’re essential. Without them, every mistake could turn into a financial disaster. A software vendor might indemnify a client against IP infringement claims. A manufacturer might indemnify a retailer if their product causes injury. The rule is simple: if you caused it, you pay for it.

The Three Words That Change Everything

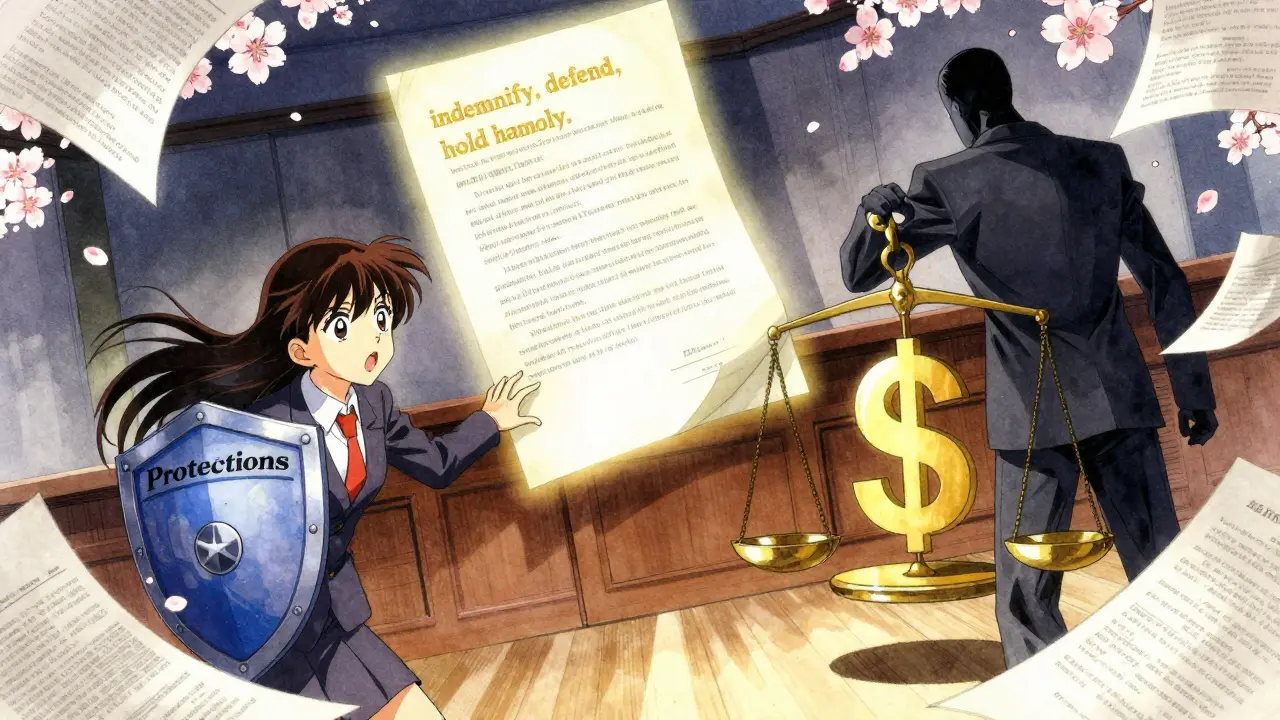

Don’t let lawyers confuse you with three similar terms: indemnify, defend, and hold harmless. They sound alike, but they mean very different things.

- Indemnify means pay for losses. If a court orders you to pay $500,000 because of the other party’s mistake, they owe you that money.

- Defend means pay for lawyers. Even before a verdict, if someone sues you because of their error, they must cover your legal fees from day one.

- Hold harmless means you can’t sue them back. If you’re protected under this clause, you can’t turn around and claim they caused your losses-even if they did.

Many contracts say “indemnify, defend, and hold harmless” as if it’s one thing. But legally, they’re three separate obligations. Courts in places like California have ruled that these terms must be treated distinctly. A vague clause won’t protect you. You need precision.

What Triggers Indemnification?

Not every problem triggers payment. The contract has to say exactly what does. Common triggers include:

- Breach of contract-like failing to deliver on a promise

- Violation of law-such as using unlicensed software or violating data privacy rules

- Third-party claims-when someone outside the contract sues one of the parties

- Negligence or misconduct-like a vendor’s poor security leading to a hack

For example: A SaaS company promises to encrypt customer data. If they fail and a hacker steals personal information, the customer gets hit with regulatory fines and lawsuits. The indemnification clause kicks in-now the SaaS provider pays for everything. That’s how it’s supposed to work.

What’s Covered-and What’s Not

Not all losses are equal. Most contracts limit what can be claimed. Two big exclusions you’ll see:

- Consequential damages-like lost profits, reputational harm, or lost business opportunities. These are often excluded because they’re too unpredictable.

- Indirect losses-such as a customer leaving because of a service outage. Courts often won’t enforce claims for these unless they’re explicitly included.

There’s also usually a cap-meaning the indemnifying party won’t pay more than a set amount. In M&A deals, this might be 10% of the sale price. In software licenses, it could be the total fees paid over a year. Without a cap, a small mistake could bankrupt a vendor.

And then there’s the deductible-the “basket.” Many contracts say: “We’ll only pay if your losses exceed $50,000.” That’s to prevent small, everyday issues from turning into lawsuits. It keeps the system from being abused.

Mutual vs. One-Sided Protection

Is it fair for only one side to pay? In most cases, yes. If you’re buying software, the vendor indemnifies you. If you’re selling a product, you indemnify the buyer. That’s because the seller usually controls the product, the code, the design-the source of the risk.

But sometimes, it’s mutual. In construction contracts, both parties often indemnify each other. Why? Because both could cause harm. If a subcontractor gets injured on-site, the general contractor might be liable. But if the client’s site manager gives unsafe instructions, the client could be at fault. Mutual indemnity balances that.

Unilateral indemnity is common when one party has more power. Big corporations often demand vendors indemnify them, no matter what. Smaller vendors don’t have much choice. But smart vendors push back-they’ll agree to indemnify, but only for things they directly caused, not for things the buyer messed up.

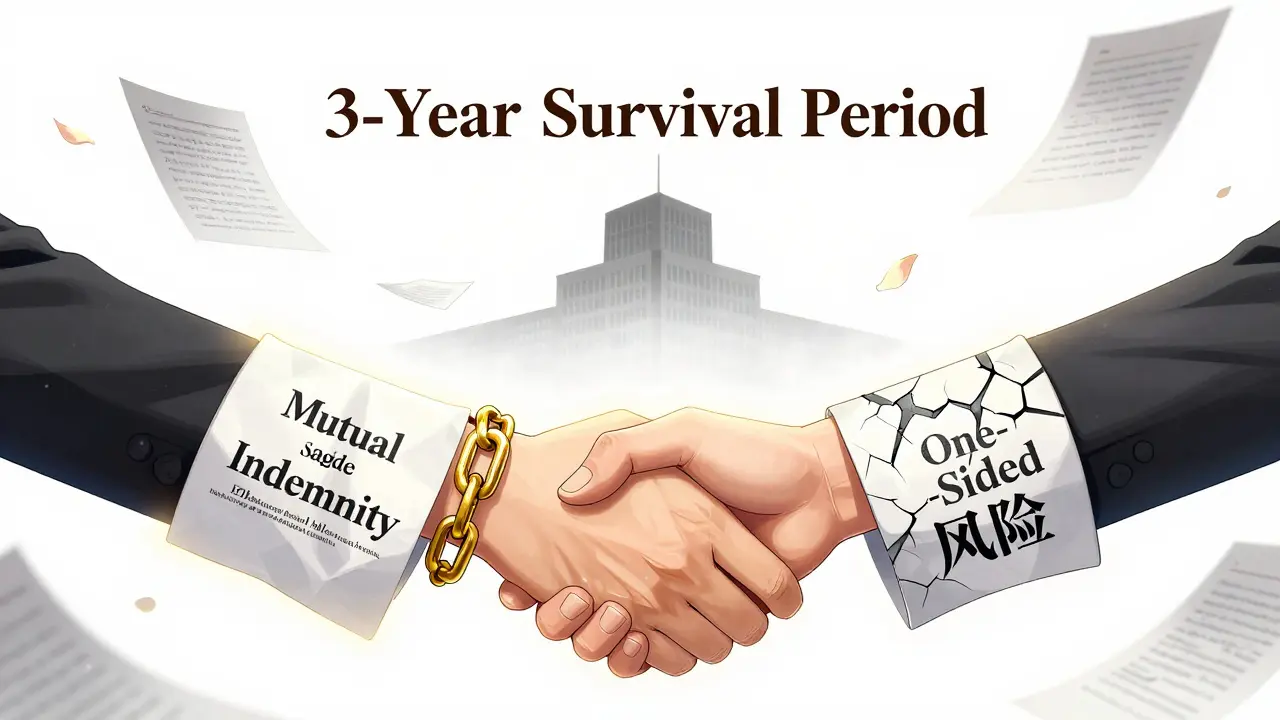

How Long Does Protection Last?

Indemnification doesn’t vanish when the contract ends. But how long it lasts depends on what’s being protected.

There are two types of promises in contracts: fundamental and non-fundamental.

- Fundamental promises are about the core of the deal: ownership of assets, legal authority to sign, tax compliance, no hidden liabilities. These usually survive for years-often 3 to 5 years after the deal closes.

- Non-fundamental promises are about day-to-day operations: employee benefits, software licenses, minor contracts. These often expire after 12 to 18 months.

This matters because if a buyer discovers a tax issue two years after buying a company, they can still claim indemnification if the seller made a fundamental misrepresentation. But if they find out the office printer lease was outdated? Too late.

What Happens When a Claim Is Made?

Indemnification isn’t automatic. There’s a process.

- You must notify the other party in writing, usually within 30 days of learning about the claim.

- You must give them control over the defense-unless you negotiate otherwise.

- They have the right to hire lawyers, settle the case, or fight it in court.

- You can’t settle without their approval, because they’re paying.

This is where things get messy. If the indemnifying party drags their feet or settles for too much, the protected party can still suffer. That’s why some contracts say: “You must defend in good faith,” or “You must use counsel approved by me.”

And don’t forget insurance. Many contracts require the indemnifying party to carry liability insurance. If a vendor claims they’ll cover your losses but has no insurance? That’s a paper promise. Always check.

Why This Matters in Real Life

Imagine you’re a small business buying a CRM system. The vendor says, “We’ll indemnify you for IP infringement.” You assume that means you’re safe.

Then you get sued because the CRM uses code copied from another company. Your legal bills hit $80,000. You ask the vendor to pay. They say, “We only cover direct damages, not legal fees.” Or, “The cap is $20,000.” Or, “We don’t cover claims filed more than a year after you started using it.”

Now you’re stuck. That’s why reading the fine print isn’t optional-it’s survival.

What to Do Before Signing

Don’t rely on boilerplate. Here’s how to protect yourself:

- Ask: “What exactly are you indemnifying me for?” Get it in writing.

- Check the cap. Is it reasonable? Is it higher than what you paid?

- Confirm the survival period. Does it match the risk? For tax issues, you need at least 3 years.

- Verify insurance. Ask for proof of coverage.

- Don’t let them exclude “consequential damages” if your business depends on uptime or data integrity.

- Insist on control over defense if the claim could hurt your reputation.

Indemnification isn’t about trust. It’s about documentation. Even if you’ve worked with someone for years, if their contract doesn’t protect you, you’re exposed.

Bottom Line

Liability and indemnification aren’t just legal jargon. They’re your financial safety net. In every transaction-big or small-you’re transferring risk. The question isn’t whether you need it. It’s whether you’ve negotiated it right.

Most people focus on price, delivery, and features. But the real cost of a bad deal shows up years later, in courtrooms and settlements. The party that understands indemnification doesn’t just sign contracts-they control risk.

What’s the difference between liability and indemnification?

Liability is legal responsibility for harm or loss. Indemnification is a contract promise to pay for that liability. You can be liable without indemnification-meaning you’re on the hook. Indemnification shifts that burden to someone else, based on what’s written in the agreement.

Can I waive indemnification entirely?

Technically yes, but it’s rare. Most companies won’t sign without it. If you’re the buyer, waiving indemnification means you’re accepting all risk-even if the seller caused the problem. If you’re the seller, refusing to indemnify could kill the deal. It’s usually better to narrow the scope than remove it entirely.

Do indemnification clauses work in all countries?

They’re enforceable in most common law countries like the UK, US, Canada, and Australia. But civil law countries (like France or Germany) handle risk differently. Some limit indemnification for gross negligence or intentional harm. Always check the governing law clause in your contract.

What happens if the indemnifying party goes bankrupt?

You’re out of luck. Indemnification is only as good as the other party’s ability to pay. That’s why insurance requirements are critical. If the contract says they must carry $1 million in liability insurance, and they don’t, you have leverage to walk away-or demand a letter of credit.

Are indemnification clauses enforceable if they’re too broad?

Courts often strike down overly broad clauses. If a contract says “indemnify for any and all claims, even those caused by you,” it may be deemed unconscionable. Courts prefer precision: “indemnify for losses arising directly from breach of warranty X.” Vague language doesn’t protect you-it invites disputes.

Anna Pryde-Smith

January 22, 2026 AT 14:23This is why I refuse to sign any contract without a lawyer reading it first. I had a vendor once say, 'Oh, it's just standard language'-then they got bankrupt after a data breach and left me holding the bag for $200K in fines. No more trusting 'standard clauses.' Read the damn fine print or get screwed. Period.

Indemnification isn't a gift-it's a shield, and if you don't check the thickness, you're just holding cardboard.

Kerry Evans

January 23, 2026 AT 17:14Actually, you're all missing the point. Indemnification clauses are only enforceable if they comply with the doctrine of unconscionability under UCC § 2-302, and courts in the Ninth Circuit have consistently invalidated clauses that shift liability for the indemnitee’s own gross negligence-unless explicitly stated in capital letters. Most people don't realize that 'hold harmless' doesn't automatically waive tort claims unless the language is unambiguous. You need to cite Restatement (Second) of Contracts § 195 if you're going to argue this properly.

Susannah Green

January 24, 2026 AT 07:40Yes!! And don’t forget-‘defend’ means they have to pay your lawyers from Day 1, not wait until trial. I once had a vendor delay for 6 months, and my legal bill hit $47K before they even showed up. Now I always insist on: ‘Defend immediately, indemnify fully, hold harmless unconditionally.’ And I underline it. Three times.

Also, if they say ‘consequential damages excluded’-ask them if they’ve ever lost a client because their software crashed during peak season. If yes, then they’re the ones who should pay for the fallout. Don’t let them weasel out.

And PS: always ask for proof of insurance. A $5M policy isn’t just ‘nice to have’-it’s your only real backup when they vanish into thin air.

Kerry Moore

January 25, 2026 AT 22:48It is of paramount importance to recognize that indemnification obligations are inherently contractual in nature and derive their efficacy from the precise articulation of terms therein. Absent clear, unambiguous language delineating the scope of indemnity, including the temporal duration, the nature of covered losses, and the procedural mechanisms for notice and control of defense, the clause may be deemed void for vagueness under the parol evidence rule. Furthermore, the imposition of a cap without a corresponding risk assessment is economically irrational and exposes the indemnitee to disproportionate liability. It is therefore recommended that parties engage in pre-contractual risk allocation modeling prior to execution.

charley lopez

January 26, 2026 AT 07:31From a compliance standpoint, the mutual indemnity structure in construction contracts aligns with ISO 31000 risk management principles-shared exposure reduces moral hazard. But in SaaS, unilateral indemnity is the norm because the vendor controls the attack surface. That said, the survival period for fundamental reps should mirror the statute of limitations for the underlying risk (e.g., tax: 3-7 years, IP: 6 years under DMCA). Cap should be tied to annual fees, not deal value. And always require a certificate of insurance with loss payee clause.

Oladeji Omobolaji

January 26, 2026 AT 21:27Man, I read this and thought-this is why I don’t do business with US companies anymore. Back home, we just say ‘you broke it, you fix it’ and move on. No 20-page clauses. No caps. No insurance certs. Just trust and a handshake. Guess I’m too old-school.

Sallie Jane Barnes

January 28, 2026 AT 18:34Thank you for writing this. I work with small startups and they always think ‘it won’t happen to me.’ But last year, one got sued over a stolen API key from their vendor’s poorly coded plugin. $120K in fines. They had no indemnity clause. No cap. No insurance. Now they’re out of business.

Don’t be that person. Read. Ask. Insist. Your future self will thank you.

Andrew Smirnykh

January 30, 2026 AT 06:56This is fascinating-especially the cultural angle. In Japan, indemnification clauses are often softened with ‘good faith’ language because the relationship matters more than the contract. In Germany, they’re stricter about gross negligence exclusions. But here in the U.S., it’s all about liability shifting. I wonder if the global rise in SaaS contracts will force more harmonization-or just more legal chaos.

Laura Rice

January 31, 2026 AT 12:16Okay I just read this and cried a little. I’m a solo founder and I signed a contract last year that said ‘no consequential damages’ and ‘cap at $5K’-and my whole business runs on uptime. When their server went down for 72 hours during tax season? I lost $80K in sales. They said ‘sorry, not covered.’

I’m not mad-I’m just done trusting ‘standard’ contracts. If you’re selling something that touches my customers? You’re liable for my losses. Period. No cap. No weasel words. I’m not asking for a favor-I’m asking for basic human decency.

Sue Stone

February 2, 2026 AT 07:46Just read the damn clause.